Standard budgeting advice assumes a predictable paycheck landing on the same day each month. For freelancers, founders, salespeople on commission and anyone with seasonal work, that assumption falls apart immediately. A great month and a lean month need to coexist in the same plan.

Budget on a floor, not an average

The instinct is to budget around your average month. Averages hide the problem: half your months fall below them. Instead, identify your floor — a conservative estimate of what you can reliably expect even in a slow month — and build your essential spending around that number.

Let good months fund bad ones

In a strong month, the surplus above your floor doesn't get spent — it gets reserved. This is where the Safe to Spend model earns its keep: instead of your balance ballooning and tempting you, the extra income is set aside to smooth out the months where you earn less.

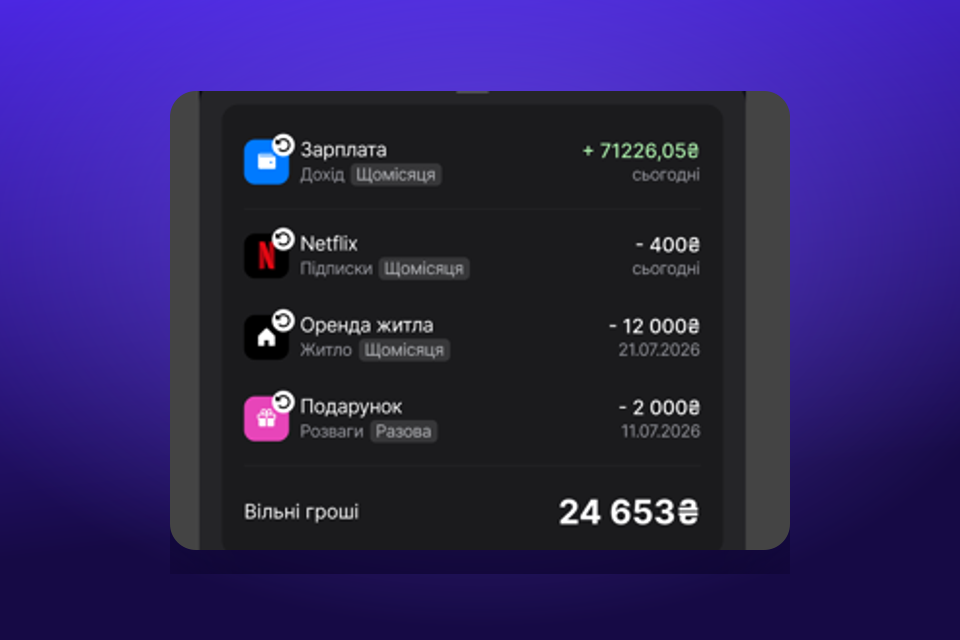

Reserve for the bills you know are coming

Irregular income doesn't make your expenses irregular. Rent, software, insurance and taxes still arrive on schedule. Enter them as planned expenses so they're reserved the moment you get paid — not discovered when they hit. For the self-employed, treating tax as a reserved expense on every invoice is the single highest-leverage habit you can build.

Separate the business from the person

If you run a business or side project, keep it in its own space. Mixing business cash flow with personal spending is how founders convince themselves they're profitable when they're funding the company out of their grocery budget. A separate space shows the real P&L of each.

Recalculate often

With irregular income, your plan is a living thing. Every time a payment lands or slips, your Safe to Spend should update. That constant recalculation is exactly what a manual spreadsheet can't keep up with — and what an app is built for.

Keep reading